The Value Ruler of M&A Theses

6 M&A theses ordered by the value created to the founder

In the game of mergers and acquisitions, some cards can unlock more value than others. In the cases we studied, the acquisitions of Plataformatec by Nubank and Zeropaper by Intuit, these differences became clear.

Is it possible to list the M&A theses in order, from the one that tends to confer less value to a target company to the one that appreciates it the most? This is the purpose of this article.

Each case is different

A generalization like this is inherently imperfect. We are talking about qualitative theses, but they are associated with the perception of the company's quantitative value. Even so, I will take the risk of this exercise by explaining the rationale behind it, which will make it easier to adapt this initial reading to each specific case.

Perspective

A value perception comparison only makes sense when we are talking about a single target company. In other words, if your company is in the aim of others with different merger/acquisition theses, each one may have a different perception of value. It is this perception that we are trying to list on a ruler. The perception of your company's value from the perspective of potential interested parties, with their theses to join forces with you.

The Theses Value Ruler

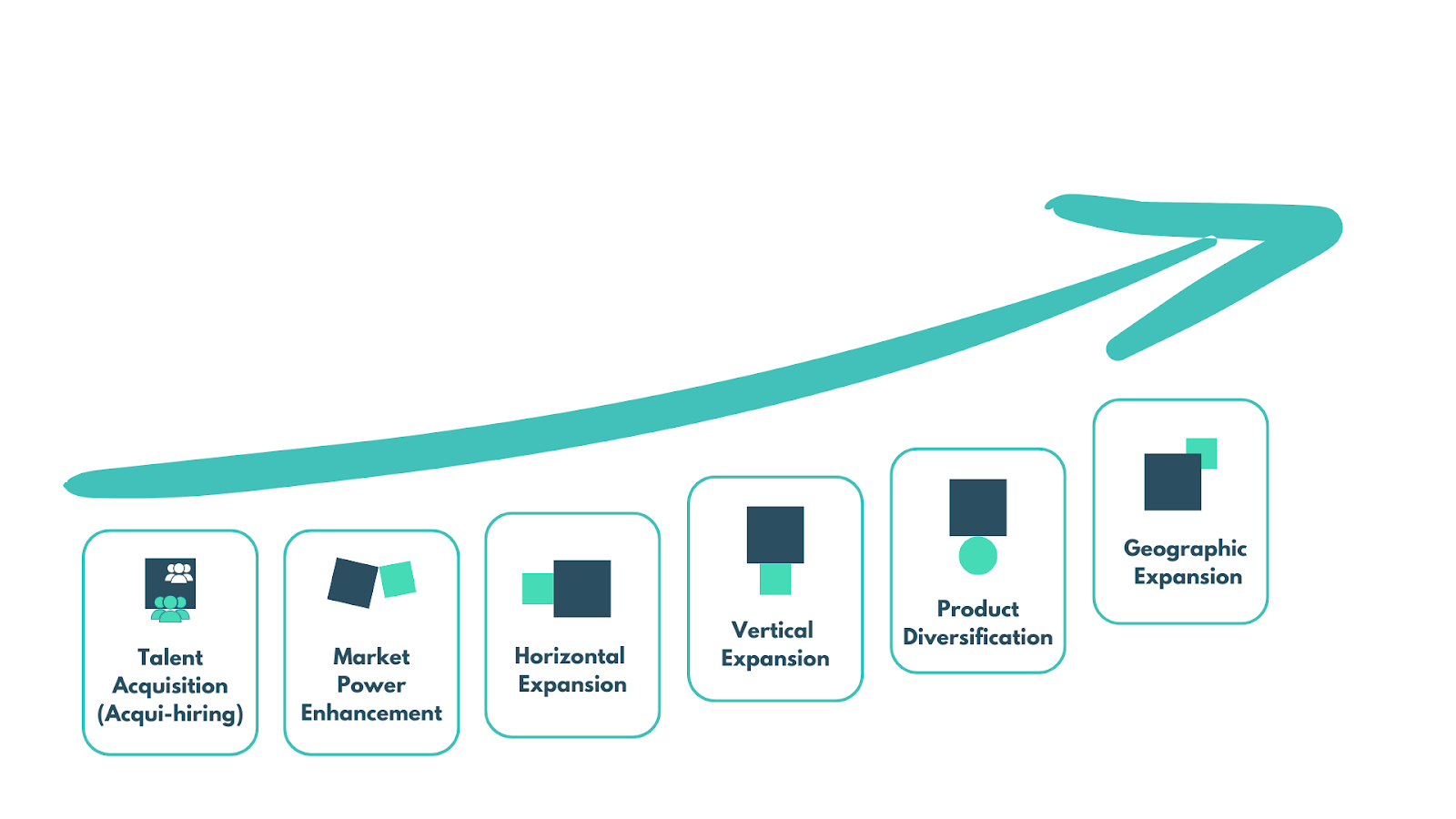

For the sake of simplicity, we will only list the 6 main theses that are most common in business. Less frequent theses, such as technology acquisition or regulatory adequacy, may vary even more from case to case, weakening our comparison.

In this image is my generic proposal for the value relationship between the thesis cards.

The further to the right, the more value the thesis card attributes to the deal. Let's go to why.

Acqui-hire

This is a talent acquisition thesis. Even though they may be quite valuable to the interested company, people tend to be seen more as a cost than as a potential source of revenue. Therefore, even if the company has relevant revenue, the motivation for bringing in a team is not to bring this revenue. It can even often be discarded.

The acquisition of Platarformatec by Nubank is the perfect example. The bank had no plans to offer technology consulting, so all revenue from the company was discontinued. In this deal, it was very important as a negotiating lever for the founders to have another thesis card, from another company interested and willing to pay a higher amount. This served as negotiating leverage.

In some cases, however, this may be the card that gives the most value to the deal, or the only relevant one. For example, in the case of a company at a very early stage, which has not even launched the product, but has a top team, any revenue multiple would earn zero valuation, but an Acqui-hire can offer an interesting price tag.

Increase in Market Power (Direct Competitor)

The purchase or merger with a direct competitor, as we saw in the case of Petz and Cobasi, reduces competitive pressure and concentrates market share. However, it is a type of transaction in which part of the original value of the business can be destroyed by operational overlaps, for example. Typically cross-sell synergies are small because we are talking about competitors competing for the same market, with the same products.

Still, in this case businesses are valued by revenue (and margin, normally). So, compared to an Acqui-hire they tend to be worth more. Imagine if Petz decided to keep only Cobasi employees, or vice versa, throwing the stores and revenue away. The operation would be worth much less.

Horizontal Expansion

This is a strategy that I experimented with in several acquisitions as M&A director at TOTVS. It represents entry into a new segment or market. In other words, it is expected that there will be little overlap and destruction of value as a result, but it is also expected that synergies will be limited, after all, we are talking about customers from different segments. Products that serve one segment well will not be the ideal fit for another.

Vertical Expansion

The purchase of a supplier or a distribution channel has an intrinsic potential for synergy, which is the increase in margin through the combination of businesses. This immediate value creation leads me to classify this type of transaction as more valuable to the buyer than a mere expansion into a new segment.

But there is a catch: this is only true if the absorbed business is maintained in full. For example, let's say that an acquired supplier has several other customers, but because they are competitors of the acquiring company, there is no interest in maintaining supply for them. In this case, part of the value of the business will be discarded and it should be seen as an Acquisition of Strategic Resources (a card that we did not bring to the analysis, but which would be close to Acqui-hire on the ruler). It is easy to understand this by thinking about the case of Plataformatec itself, whose contracts with customers were gradually discontinued to only serve Nubank.

Product Diversification

If done well, an acquisition of a new product line can unlock enormous potential for value in cross-selling and other synergies. What differentiates Product Diversification from Horizontal Expansion is precisely the overlapping of customer segments, ideally with low overlapping of the customer base. In other words, the product of one company can be sold to the customer base of the other and vice versa.

As perfect persona segmentation in B2C is more difficult than in B2B, I tend to consider acquisitions in B2C more as product diversification than horizontal expansion.

The best example in history was probably Google's acquisition of YouTube. The company was acquired in 2006 for US$1.65 billion and in 2023 it earned US$31.5 billion, around 10% of Google's total revenue. In a simple rule of three with Google's 2023 Market Cap, YouTube would be worth around US$175.6 billion. Not bad for product diversification.

Geographic Expansion

The case of ZeroPaper, acquired by Intuit to enter Brazil, is iconic in the perception of value that this thesis card can bring to the game. Premium subscribers who have access to valuation data can understand that the revenue multiple paid by Intuit in this case is stupid.

Why does this make sense? Entering a new country by establishing an operation organically is expensive and time-consuming. When it comes to Brazil, it is still very risky. Considering that normally entering a new territory is to sell the original product, in a similar segment, but in another geography, all the possible synergies of the previous theses can apply. Added to this are time savings, cost and risk reduction.

The Ultimate Arrangement

The order of these cards can vary greatly. The most important thing is to examine the synergy rationale of each interested company's theses. The greatest usefulness of this analysis, however, lies in the possibility of generating value through the comparison of cards from different interested parties. Let's dive deeper into how to do this.

Playing with the Cards

Keep reading with a 7-day free trial

Subscribe to Exit Strategy to keep reading this post and get 7 days of free access to the full post archives.