The Mathemagic of Entrepreneurship

How entrepreneurs create companies that are worth millions

Entrepreneurship is about building something much bigger than yourself, capable of transforming the world by uniting people around a purpose of achieving great things that a single individual could not. That was the basis of my vision and my ambition to build a business.

You need to have a bigger reason to embark on such a challenging and risky journey. But it turns out that entrepreneurship is about all of this and much more.

The mathematics of value construction

When I entered the world of M&A I started to see another side. The creation of value through the construction of a company is measurable, especially when this company is valued by a third party who intends to acquire all or part of it (such as a venture investor).

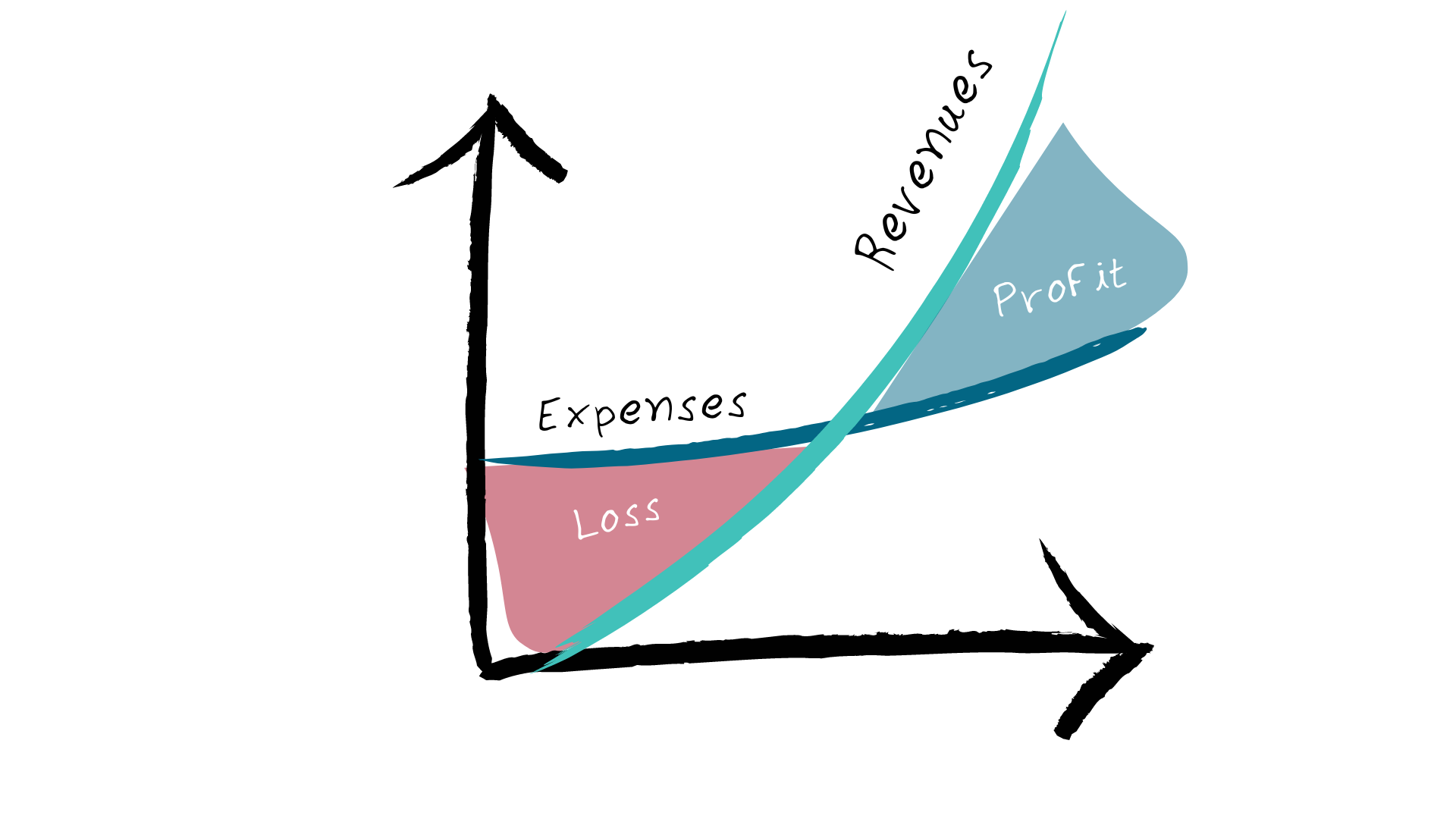

I learned to value companies using classic valuation tools at a moment in time and space where a loss-making company did not generate value. It may not seem obvious now, but that time existed. Companies were evaluated based on their discounted cash flow projection. In other words, a projection of how much money it would be able to generate over the years and how much it is worth today. Without wanting to make this text too theoretical, we are talking about basic financial mathematics of net present value with a discount rate. A calculation that you can do in your Excel.

But then came Jeff Bezos and his letters to investors saying that Amazon would not be profitable for many years and yet seeing the share price appreciate incredibly with the company's growth. And after that, many others from the Uber generation.

Cases like these made the financial market and "mortal" investors understand the way a venture capitalist sees value in a company that grows even though it loses money.

"Everything is worth what your buyer is willing to pay"

Publilius the Syrian

Was that good? In my opinion, yes. Today, we have many more investors with the maturity to see value in startups, whether acting as angels or through a proliferation of investment funds. More people effectively investing money in entrepreneurship means more value generation.

Emotional value and mathematical value

I talk a lot about building value perception through desire to purchase at all stages of the Most Valuable Product Journey. But today we are going to talk about mathematical value. Or rather, mathemagical.

To begin with, it's worth saying that discounted cash flow is not dead. In other words, if your company has the capacity to generate cash and projections indicate that it will continue to do so, it has value. In the current economic situation, this has once again gained enormous importance. But even if it is not yet a money-generating machine, there are several other sources of value for your company.

The value ruler

In "The Value Ruler of Mergers and Acquisitions" we compare the sources of value perception of different M&A theses, ordering them according to this criterion.

Diving deeper into this concept, let's dissect the sources of monetary value that can be considered in an M&A valuation:

Assets

Assets have an intrinsic and relatively static value. A company can be acquired only for the value of its assets. But if it has liabilities (debts) they are also deducted from its value.

In the rule we only list "Acqui-hire" as a type of transaction based on "assets" (in this case the intellectual assets of the team that makes up the company), but we mention other types such as the acquisition of strategic assets and technology. If your company has zero revenue, it could still be an M&A target if assets like this are of interest to other companies.

Revenue

Many companies are valued by a revenue multiple. In segments or stages where it is common for companies not to make a profit, such as in a series A round of venture capital, revenue is one of the main evaluation rulers.

When Amazon and Uber were not yet profitable, but were already worth billions of dollars, the ability to generate revenue was one of the great justifications. All of the ruler's M&A theses based on increasing market power are based on incorporating revenue.

In the next sessions we will go deeper into potential revenue multiples.

Growth

The growth potential of this revenue provides additional value. Honestly, a company with a negative margin and without growth is not worth much, but growth can change that.

Growth brings gains in scale and therefore the perception of value is often linked to the understanding that with growth may come cash generation.

Profit Margin

Finally, profit margin is the oldest way of valuing a company. When we talk about cash generation, the margin is an assumption. The tendency is for a company that has a good margin to have a higher value than one with similar revenue in the same sector that makes a loss. But if other factors such as low growth are associated, this may not be true.

The margin that is often used to evaluate companies is EBITDA (Earnings Before Taxes, Interests, Depreciation and Amortization) and the multiples can be up to an order of magnitude greater than the revenue multiples.

The business case for venture capital

The main objective of a company that receives venture capital investment is to grow as much as possible, as quickly as possible. A company like this shouldn't even have a positive margin. Therefore, if it is possible to reinvest the margin to grow further, it should do so.

The bet is that by growing a lot and ideally dominating its market, this company will be in a privileged position to generate cash in the future. And this bet on the future is enough for one or more investors to attribute value to it at the current moment.

With cash generation (or at least this potential) this company will be positively evaluated by the financial market in an IPO transaction, or it can be acquired for a substantial value, according to the ruler's theses.

So the mechanics are: invest now, make the company grow (revenue) even without profit to the point where it has gained enough scale to generate a large profit and be worth a lot of money.

With some variations this is typically the case for a venture capital investment (in a company1). This is the case of Uber and Amazon, two notable examples that we have already mentioned here.

Value invested versus value built

A didactic way of studying the mathematics of value creation in building a company is to compare the value invested in it with the value created. For this we will use some Benchmarks.

Uber

Over its history as a private company, Uber has raised $22.2 billion in 20 rounds of financing. The company reached a valuation of US$82.4 billion in the IPO (just under 4x the amount invested), through which it raised another US$8.1 billion. Today the company has a market value of 144 billion dollars (almost 5 times the total amount invested).

Airbnb

Airbnb raised a total of US$6 billion until the IPO in which it reached a valuation of US$20 billion (3.33 times the amount invested).

Today this valuation is 94 billion, more than 15 times the investment.

These can be considered extreme examples. Even more extreme is the return on investment calculation of those who entered in the early rounds. The point here is that the company is an institution that has the potential to multiply the capital invested in its own construction, attributing value to itself along the way.

Now that the investor's perspective is clear, let's dive deeper into the entrepreneur's perspective.

The mathemagic of the entrepreneur

Let's start with a simple case. A bootstrapped company with just one founder. Let's assume you are the founder and started by providing services. A specialized consultancy, say in marketing. Customers liked the service and asked for more projects. You hired more people, grew the business and after ten years it reached a revenue of 10 million dollars per year.

Impressive, congratulations! As a solo founder, the company is 100% yours. Every month you can take 12% of the company's revenue as dividends. US$ 120 thousand. Not bad!

Then you receive an acquisition proposal. What is a fair valuation? The answer is always it depends, but I want to invoke an anecdote that I heard before entering the world of M&A.

"The baker decides to buy his competitor's bakery. He asks to stay at the counter to learn about the operation before making an offer. The competitor agrees and he spends the day serving customers. At the end of the day, he closes the cash register and calculates the day's revenue , multiply by the number of days of the year in which the business operates and make an offer in this amount."

What does this imply? In saying that companies are often valued by a multiple of revenue and that 1x annual revenue is a starting ballpark for that number. I'm not promising that your company is worth this, more than that, or less, but it's a good place to start making a "baker's account."

The sky, however, is the limit. Airbnb, for example, is worth more than 11 times its annual revenue. Uber, a little less than 4 times. Microsoft more than 13 times.

But let's say that for your Marketing consultancy, 10 million (1 times annual revenue) is a fair value. You will (let's assume) put all this money in your pocket at once. If you continued making your monthly withdrawals of 120 thousand, you would need more than 83 of them to accumulate that amount.

You know what else? You'll have time to start another business and build that value all over again.

Mathemagic, right?

Some Buts

Maybe this isn't the best decision. Even if the price is fair, if you are motivated to continue running the business and it is growing, in a short time it could be worth twice as much. It may be a long time in absolute terms, but very short compared to the entire journey you've had so far.

Level growth

When a company reaches a certain value level and continues to grow, its value is also growing proportionally. So if your company took 3 years to double its revenue when it made one million and it still takes 3 years to double with 10 million, now in those three years you build much more value than starting a new (similar) company from scratch.

Risk

Building a company is very risky. Success rates are very low, less than 10%. Our biased brain only pays attention to the beautiful stories of those who worked. It's called survivorship bias: whoever shows up to tell the story is one who survived, which is why we tend to think that most stories have a happy ending. This implies that it's hard for us to think about the failure scenario, but its chances are greater than those of other outcomes.

To assess whether entrepreneurship is for you, you need a good dose of reality.

When might it not be worth it?

Let's say you're a high-earning executive. You look at the calculation we made and think you can earn 10 million in 10 years as an entrepreneur. Now, if the statistics are generous, this scenario will be 1 in 10. In other words, the expected value is 1 million. In 10 years. Then things don't get so interesting anymore, do they?

Try to leave your confirmatory biases aside and analyze the risk carefully.

Lower risk scenarios

When you and your partners bring relevant assets to the business they can reduce the risk of failure. These assets may include specific knowledge about the segment they are entering, network of contacts, commercial capacity, among others.

It is important, before making the decision to undertake the mathemagic, to evaluate the real risks of the business and how the group of partners is mitigating them.

Including venture capital in the math

Venture capital complicates the whole calculation. I don't know if I'll be able to keep it simple, but I'll try.

Venture investors contribute capital to the company in exchange for a stake. This means that when you go through an investment round it will be diluted by around 20% (you will have 20% less of the company) which will be handed over to new investors.

Over multiple rounds, founders are successively diluted.

A study from SaaStr analyzed a set of companies that raised VC and made an IPO and concluded that on average the founders had 20% of the business, that is, one fifth of the initial stake.

On the other hand, business growth is accelerated and the level it can reach with this acceleration is greater. The VC's goal is usually to take its investment to a billion-dollar valuation.

The calculation for the founder is more or less like this: you will have a fifth of a company that could be worth 10, 20, 40 times more. A smaller slice of a larger pie (or watermelon). It's mathemagic on steroids.

The risks remain on all sides. If there's one thing that an injection of venture capital doesn't promise, it's increasing your chances of survival. So it's just about raising the level of the game. That is, of course, if your business is VC-fundable, but that is a topic for another time.

Conclusion

Building a business is extremely risky, but it can bring a financial return that is unmatched by other career possibilities. The chances, however, are low of this happening. Studies show that entrepreneurs accumulate less wealth on average than their peers who pursue a corporate career.

So going back to the beginning, it only makes sense for you to undertake if you really want to build something much bigger than yourself, capable of transforming the world by uniting people around a purpose of achieving great things that a single individual could not achieve.

I do not propose to explain the business model of a VC fund here, which is governed by another, more sophisticated mathematics.